The specific enabling law of each operation carries the equivalence formula. As a rule, a CEPAC does not correspond to a single fixed square meter. It is worth a variable number, according to two axes: the sub-sector of the operation and the purpose of the additional potential.

The same certificate may equal two square meters in a peripheral residential sub-sector, or one square meter in a central mixed-use sub-sector. The difference is public policy design. The municipality calibrates the rate to steer investment.

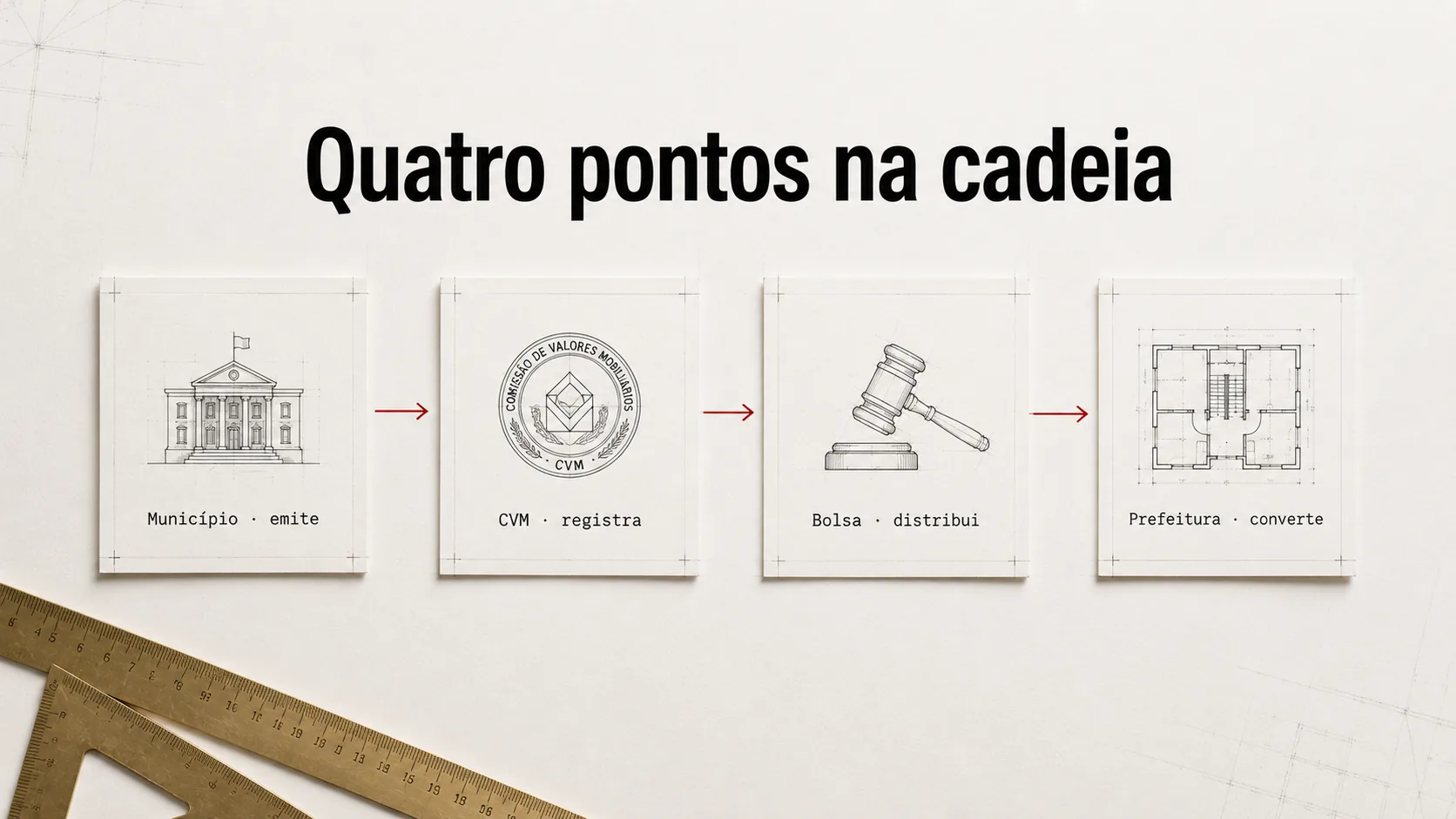

When the project is filed for approval, the developer presents the quantity of CEPACs equivalent to the area exceeding the general parameters. The municipality writes down the inventory, takes the certificates, and issues the building permit. At this moment, the CEPAC ceases to exist as a financial security. It has been absorbed into the permit.